- ESO's Monthly Start-Up

- Posts

- ESO's Monthly Start-Up

2025 Year in Review

While 2025 didn’t bring back quite the fundraising and liquidity markets that we were hoping for, there is a lot to be excited about with VC going into 2026 with the momentum building. Thank you to the Pitchbook NVCA Venture Monitor for much of this data. While there definitely we some positive trends during the year, most of it was highly concentrated.

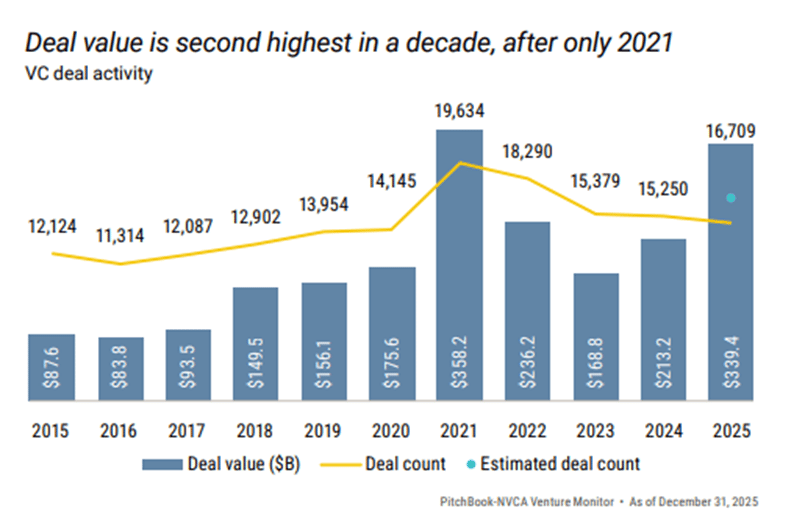

The first thing we want to touch on is deal making, with deal value having been the second highest in a decade. However, this number is slightly misleading given that a small number of outsized transactions captured a large share of capital. If your guess was AI companies, you’d be correct!

OpenAI had a $40 billion raise in Q1, Anthropic raised around $15B in Q4, and xAI captured another $10 billion in Q2. The money going into AI has truly been extraordinary, driven by a combination of both the capital intense nature of the AI development cycle and strong investor conviction. AI alone accounted for over 65% of total deal value and almost 40% of total deal count.

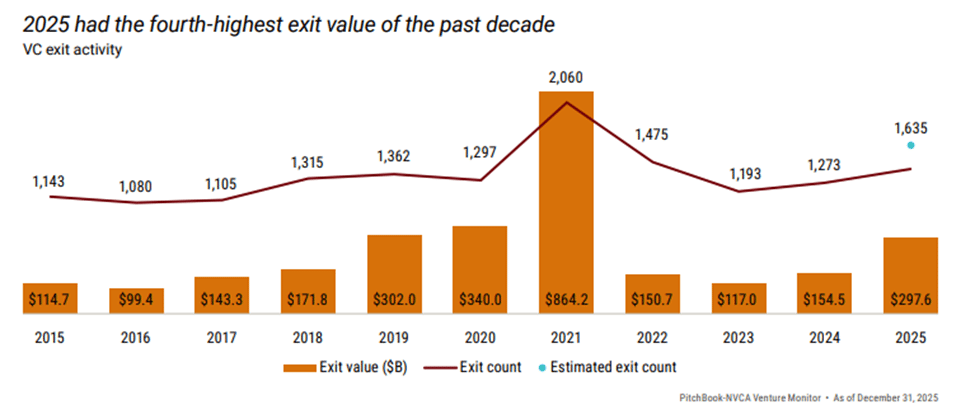

On the exit side of things, activity has been improving but trailed the high hopes that many had for the year. It was the second-most-active year by exit count and the fourth by exit value (after 2019, 2020, and 2021), generating $297.6 billion across an estimated 1,635 exits.

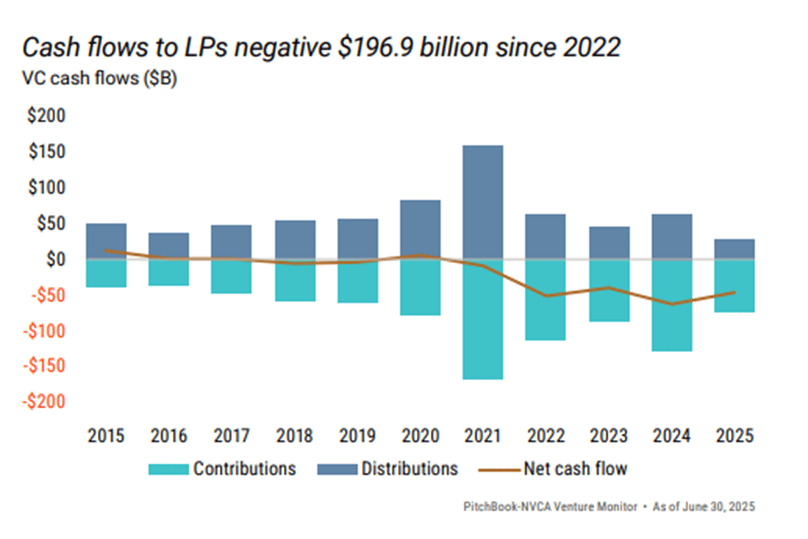

Despite the uptick, distributions were unable to offset the years of negative cash flow to LPs. Fundraising reflected this tension: 2025 saw the fewest funds closed in a decade, with capital consolidating among large, established managers and dry powder aging across vintages. Venture secondaries quietly emerged as a critical release valve, approaching parity with IPOs and acquisitions in exit value and becoming an increasingly institutionalized part of the ecosystem.

What Does All This Mean For 2026?

Selective momentum, not a flood. We are far beyond the rising tide lifts all boats environment of 2021 and into a more nuanced recovery. AI will remain the dominant capital magnet, with large, well capitalized firms continuing to control pricing and access at both the early and growth stages. However, the persistence of venture growth rounds signals that liquidity timelines are still being extended rather than resolved, lending to a slower recovery in fundraising and liquidity despite continued deal making strength. As a result of this, secondaries are poised to expand further as valuations stabilize, interest rates ease, and both LPs and employees seek liquidity without waiting for traditional exits.

In short, we are expecting 2026 to look less like a return to the old venture cycle and more like a structurally different market: fewer winners, larger checks, longer hold periods, and alternative liquidity mechanisms playing a permanent role.

Tips of the Trade

A section where we provide helpful tips for anyone with stock options or shares at private companies.

Understanding “ROFR” (Right of First Refusal)

What is ROFR?

A Right of First Refusal (ROFR) means the company and its investors are always first in line to buy your shares before you can sell them to anyone else.

ex: If you find a buyer willing to pay $10/share, you must notify the company. They have the right to buy those shares from you at that same $10 price.

Why do companies have ROFR?

Namely, Cap Table Control. ROFR allows companies to prevent "outsiders” from appearing on their list of shareholders and owning a piece of the company. This keeps ownership “in the family” by allowing the company or existing investors to increase their stake.

Impact on Employees

From a sellers perspective ROFR isn’t an issue at face value - if you are selling you don’t care who the buyer is.

For the buyer it can often lead to cold feet. Many secondary buyers are hesitant to spend weeks on due diligence and legal fees if they know the company can simply snatch the deal away from them at the last second.

Often buyers will only make formal offers if the employee can get confirmation that the company will not ROFR. This creates a chicken and the egg issue, where many times you must submit a formal Stock Transfer Agreement to find out if the company will ROFR. This often leads to stalemate where nothing happens. To get over this issue, some buyers or brokers will charge a “break up fee” so they are still compensated in the event the company exercises ROFR. Either way, ROFR requires formal notice to the board and typically delays a deal up to a month. Even if the buyer is ready to wire the money, you must wait for the company to formally “waive" or “exercise” their right.

Transfer Restrictions: Note that a ROFR is different from a total "Transfer Restriction." A ROFR allows a sale (eventually), whereas some companies ban secondary sales entirely without Board approval.

Understanding the ROFR is less about who ends up with the shares and more about managing the timeline and "deal fatigue" that comes with a secondary sale.

Funding your option exercise can be expensive and a require a large capital outlay. Feel free to reach out to us to discuss your options for partnering with ESO to exercise your options risk-free.

ESO Fund does not provide legal, financial, or tax advice.

December's Top Ten:

AI Evaluation Startup LMArena Valued at $1.7B

AI evaluation startup LMArena raised $150 M Series A at a $1.7 B valuation just four months after launching its product, signaling fierce investor interest in third-party model evaluation tools that benchmark real-world performance across multiple tasks.

xAI Raises $20B

Elon Musk’s AI company xAI raised a massive $20B in an upsized Series E, exceeding its original target and fueling expansion of compute infrastructure, model development, and data center scale as it competes aggressively with other frontier AI players.

Anthropic to Raise $20B at a $350B Valuation

Anthropic is reportedly in talks to raise roughly $20B at a roughly $350B valuation, underscoring continued investor confidence in high-growth AI builders even after massive prior financings. The company signaled their full-year 2026 revenue forecast could reach $18B.

Strava Files Confidentially for IPO

Fitness network Strava filed confidentially for an IPO, marking renewed public market interest in consumer tech brands with sticky user engagement and subscription revenue streams.

Lambda Labs in Talks to Raise $350M Ahead of IPO

ML infrastructure player Lambda Labs is reportedly in talks to raise about $350M ahead of an IPO, positioning itself as a provider of GPU-optimized hardware and software stacks for next-gen model training.

Cerebras in Talks to Raise $1B at a $22B Valuation

AI hardware specialist Cerebras is reportedly in talks to raise ~$1B at around a $22B valuation as it expands its wafer-scale computing and inference platform ahead of an eventual public listing.

OpenAI on track to top $13B in revenue

OpenAI is on track to surpass $13B in annualized revenue, putting it in rare territory relative to historical SaaS growth curves. The pace matters less for precision and more for anchoring what platform-scale AI economics now look like. The company is reportedly planning for a potential Q4 2026 IPO which would likely be the largest US IPO valuation ever (Alibaba $168B).

C3.ai in Talks to Merge with Automation Anywhere

Enterprise AI vendor C3.ai is reportedly exploring a merger with automation specialist Automation Anywhere, combining predictive analytics and workflow automation capabilities to compete more effectively against larger cloud platforms.

Capital One Buying Brex for $5B

Capital One agreed to acquire fintech Brex for approximately $5B, expanding its digital banking footprint and adding Brex’s suite of corporate cards and spend management products to its core offerings.

Spring Health Buys Alma

Mental health benefits platform Spring Health acquired employee support provider Alma, consolidating care coordination services in the workplace wellness segment and signaling deal activity in health-tech niche verticals.

Why It Matters:

January reinforced just how quickly capital is concentrating around frontier AI, compute, and platforms with credible paths to scale and liquidity. Mega rounds, eye-watering valuations, and rising revenue forecasts signaled continued investor willingness to underwrite category leaders, while a growing number of late-stage companies quietly lined up IPOs or pre-IPO financings in anticipation of reopening public markets. At the same time, consolidation across fintech, healthcare, and enterprise software highlighted a shift from experimentation to integration, as incumbents and scaled startups alike moved to own distribution, infrastructure, and workflows ahead of what looks like a more selective but functional exit environment going into 2026.

About ESO Fund

ESO Fund empowers startup employees to turn their stock options into reality. Since our inception in 2012, we've been dedicated to providing risk-free funding for the exercise of stock options, ensuring that individuals can seize the opportunities embedded in their equity.

Our mission is simple: to make equity compensation accessible and understandable. Through our innovative solutions, we've assisted countless individuals at 650+ companies in realizing the full value of their stock options, contributing to the success stories of numerous startup employees.

For more information on ESO Fund and how we can help fund your option exercise, please refer to our website at www.esofund.com!